Family Fortunes: a long-run perspective on the value of family leadership

by Michael Aldous and John Turner

8 April 2024

Disclaimer: The views, thoughts, and opinions expressed in this blog post belong solely to the guest author and do not necessarily reflect the policies, position, or views of the Family Business Research Foundation.

Our new book, The CEO: The Rise and Fall of Britain’s Captains of Industry, examines the role of corporate leaders in Britain’s economic development in the twentieth century. The book draws on a database of 1,400 CEOs to explore who gets to the top of the career ladder, what they do in the role, and analyses the effect they have on the companies they lead and the wider economy. In this article, we draw on insights from the book to discuss the changing fortunes of family business leaders.

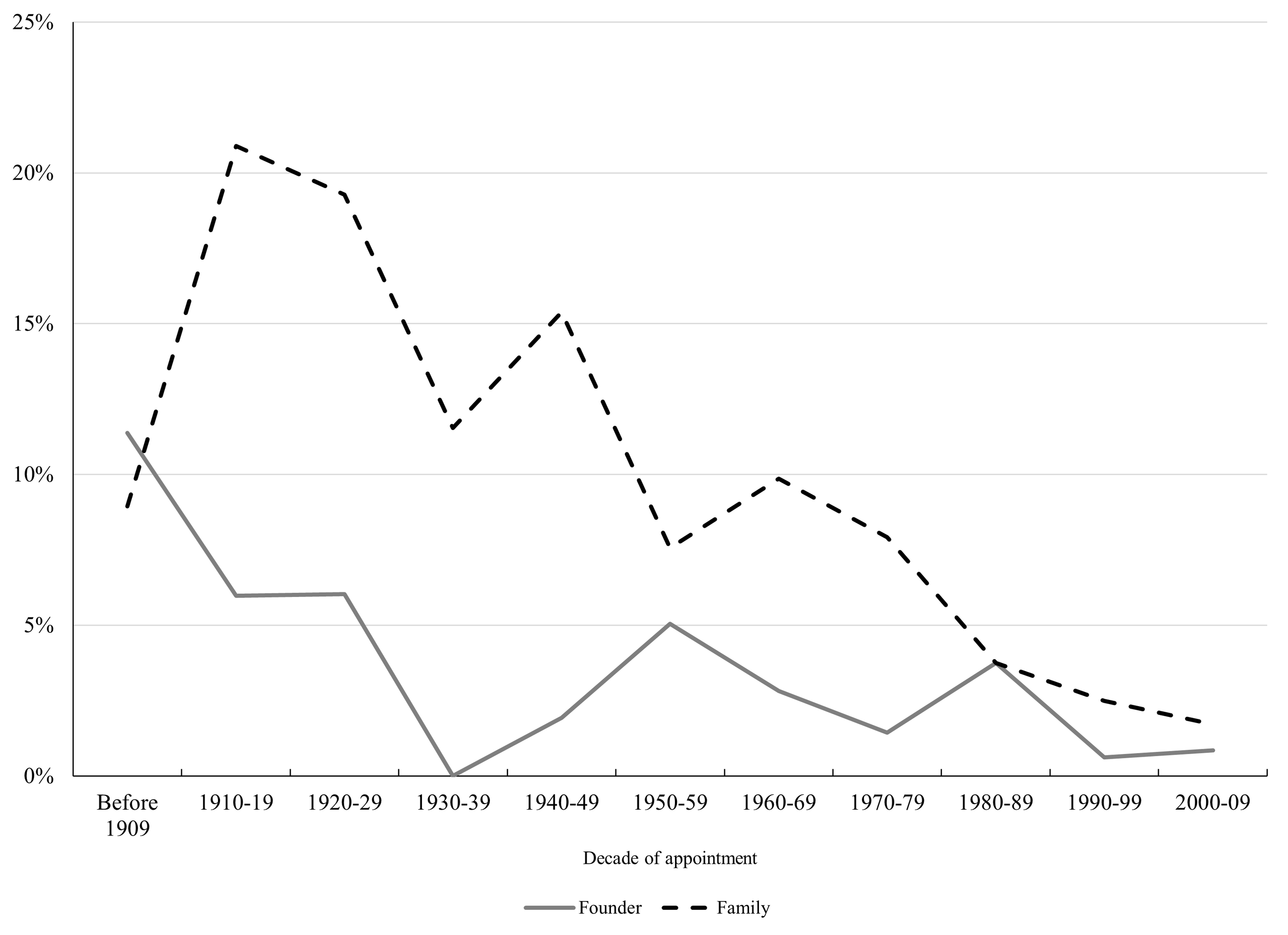

Figure 1 shows how the percentage of Britain’s largest companies that had CEOs who were family members or founders has changed over time. In the early decades of the twentieth century, about 30 per cent of Britain’s largest public companies were dominated by families or individual owners. Between 1910 and 1930, the leaders of around 20 per cent of these companies were related to their predecessors, often part of multi-generational dynasties related to the original founders (Adams et al., 2024). Some of the family-owned and -managed businesses that emerged in these years were amongst Britain’s largest and most successful companies. But, by the 2000s, this proportion had declined to less than five per cent (Adams et al., 2024).

Figure 1: Percentage of Britain’s largest companies that had CEOs who were family members or founders (pre-1909 to 2009)

Source: Adous and Turner (2025)

Why were family owned and led businesses so prominent amongst Britain’s largest companies in the early decades of the century, and what caused this decline?

The Golden Age

By the 1930s, British family-owned companies such as Guinness, Courtaulds, and J&P Coats, and some with strong family ties such as ICI and Unilever, were amongst the largest companies in the world. Indeed, family-led companies were on average larger by market capitalisation than their domestic competitors. Why had they proved so successful?

Small family businesses played an important role in the formation of these business leaders. William Lever, founder of Lever Brothers (later Unilever), learned the rudiments of business working in his father’s grocery store. Understanding of products and customers, the operations of the business, accounting and finance were all learnt in these early years. Working in a family business was a common starting point to many business leaders’ careers in the years before World War II. Families played a crucial role in equipping them with education, training, and business experience.

Before the widespread availability of finance through capital markets, family networks also played a vital role in providing access to finance. In the case of William Lever, the capital for the first soap factory that would transform Lever Brothers into a global giant was raised from within the family. Ultimately, family networks were often crucial in providing human and financial capital critical to the formation and expansion of these companies.

The Decline

Some family-owned and led companies achieved significant success over sustained periods of time, in part because far-sighted leadership and family networks enabled the development of suitable candidates for succession. But the intergenerational transfer of ownership and leadership was a significant challenge for many. Various ‘succession traps’ brought down even the most successful companies.

One trap is encapsulated in the adage ‘clogs to clogs is only three generations’, which describes how families over time lose the capabilities and motivations to run their businesses. Each generation becomes more complacent and insular than the last.

The second trap was the ‘founder’s shadow’, that is, the founder’s struggle to relinquish control over their companies. Identifying suitable successors and having the self-control to let go of a life’s work often proved difficult. There was limited interest in developing cadres of young managers and difficulties in identifying and grooming successors, as well as family rifts and the lack of interest of younger generations. This meant family business empires that did not win the genetic lottery of talented and predisposed heirs were sold off.

Several other factors also played into this decline. Waves of mergers in the interwar years and 1960s, fuelled by efforts to achieve economies of scale and diversification, saw many family- and founder-owned firms integrated into larger business entities (Hannah, 1976). Amongst family companies which survived, family control was often diluted through the sale or issuance of shares to raise capital to pursue their own mergers. Concurrently, the scaling up of companies through mergers and the growth of capital-intensive industries caused the size of the largest industrial companies to increase significantly. As these large industrial companies and capital-intensive industries came to dominate the economy, the scope for family-owned and led companies to achieve this scale was restricted.

Why does this matter?

Some historians argue that the prevalence of family ownership in Britain encouraged patronage and nepotism, which in turn led to insularity and risk aversion (Landes, 1969). Family-owned and -led companies were less willing to recruit external professional experts or adopt modern organisational and managerial structures. They failed to invest deeply in technology and other sources of innovation, which restricted their capacity to grow (Chandler, 1990; Keeble, 1994). As a result, family companies became uncompetitive and unproductive and a source of Britain’s economic underperformance. Things improved when salaried professional managers replaced family leaders and ownership was diffused to wider groups of shareholders.

However, in The CEO, the value and importance of family leadership have been significantly revised. Family ownership meant that family leaders had plenty of skin in the game. This motivated them to manage assiduously and develop the business. Similarly, leading a company with the intention of passing it on to future generations could reorient motivations away from short-term profitability to longer-term aims. For example, the Brunner and Mond families founded the chemical company Brunner Mond and Co. in 1873. Multiple generations of both families led and acted as senior executives through the company’s transformation into the global giant ICI, with the last Mond exiting the company in 1947. Familial bonds helped family leaders build trust within the company and with other stakeholders. Consequently, family leaders typically eschewed the short-termism that marked those in diffusely owned public companies.

These motivations could provide clarity and stability to the decision-making. Rather than act conservatively, family- and founder-led companies such as Brunner Mond and Co., Marks and Spencer, and Rowntree adopted innovative approaches to R&D. They spent heavily on technology and rapidly embraced innovations in marketing, retail, and product development. They were also at the forefront in engaging with new principles of scientific management that improved working practices and labour relations.

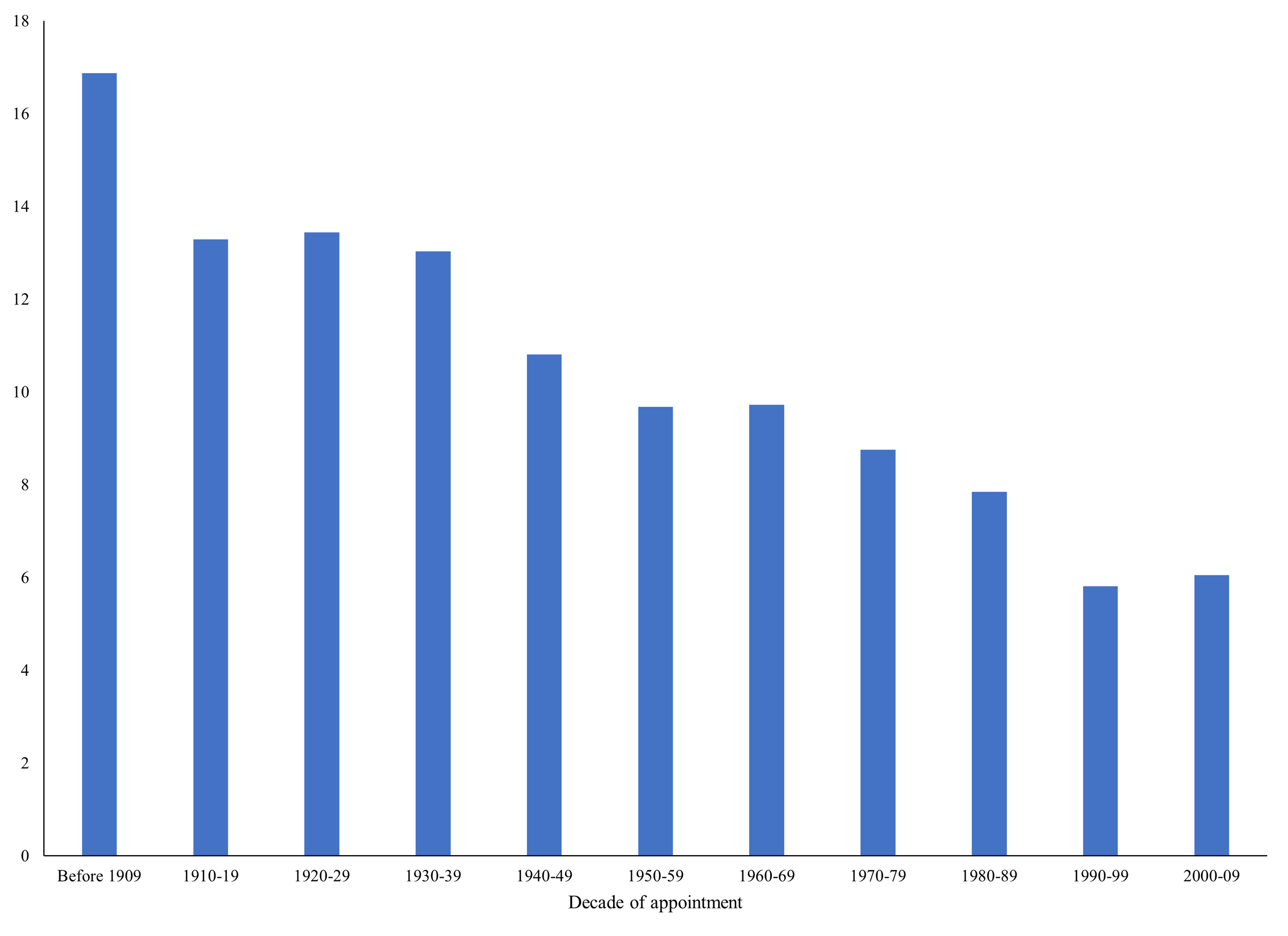

The average tenure of CEOs of Britain’s largest corporations have fallen across the century and is now under six years, whilst the probability of dismissal for poor performance is over 40 per cent (Adams et al., 2024) (see Figure 2).

Figure 2: The Average tenure (years) of CEOs (pre-1909 to 2009).

Source: Aldous and Turner (2025)

These pressures mean their focus is increasingly short-term, whilst diffuse and passive shareholder ownership has often led to divergent interests. This has serious implications for long-term strategy making, motivation to innovate, commitment to investments, and ability to lead change. As The CEO shows, the value of long-term stewardship and trust found within family leadership models provides important antidotes to some of the most pressing challenges facing business leaders today.

About the Authors

Michael Aldous and John Turner are authors of The CEO: The Rise and Fall of Britain’s Captains of Industry (Cambridge University Press, 2025).

Michael Aldous is Senior Lecturer in Management at Queen’s University Belfast.

John Turner is Professor of Finance and Financial History at Queen’s University Belfast. Both are Co-Founders and directors of the Long Run Institute.

For a more detailed account of the the historical research underpinning this article, you can view Michael’s recent LSE lecture: The Rise and Fall of Britain's Captains of Industry.

References

Adams, R., Aldous, M., Fliers, P., & Turner, J. (2024) British CEOs in the Twentieth Century: Aristocratic Amateurs to Fat Cats? Business History Review, 98(2), 359-387.

Aldous, M. & Turner, J. D. (2025). The CEO: The Rise and Fall of Britains Captains of Industry. Cambridge University Press.

Chandler, A. (1990). Scale and Scope: The Dynamics of Industrial Capitalism. Belknap Press of Harvard University Press.

Hannah, L. (1976). The Rise of the Corporate Economy. John Hopkins University Press.

Keeble, S. (1992). The Ability to Manage: A Study of British Management 1890– 1990. Manchester University Press.

Landes, D. (1969). The Unbound Prometheus. Cambridge University Press.